Blog By: Luke Glasscock

In 1933, the first “Farm Bill” was passed with “the goa[l] of ‘limiting crop production, reducing stock numbers, and refinancing mortgages with terms more favorable to struggling farmers.’”[1] In other words, the bill began the long-standing legislative practice of establishing a “safety net” for farmers.[2] Similarly, in 1938, the first Federal Crop Insurance Act was passed with the goal of promoting the national welfare and agricultural economic stability.[3]

Then, in 2014, a shift occurred; that year’s Farm Bill eliminated the system of direct payment subsidies and created two new coverage types—price loss coverage and agriculture risk coverage—and importantly cemented the federal crop insurance program as the core tenant of the modern agricultural safety net.[4] Whether or not normatively preferable to the direct subsidy regime, the spirit of the laws that formed those foundational safety nets, intended to keep struggling farms afloat and commodity markets balanced, has given way to the entrenchment of a federal insurance regime that disproportionately benefits large operations.

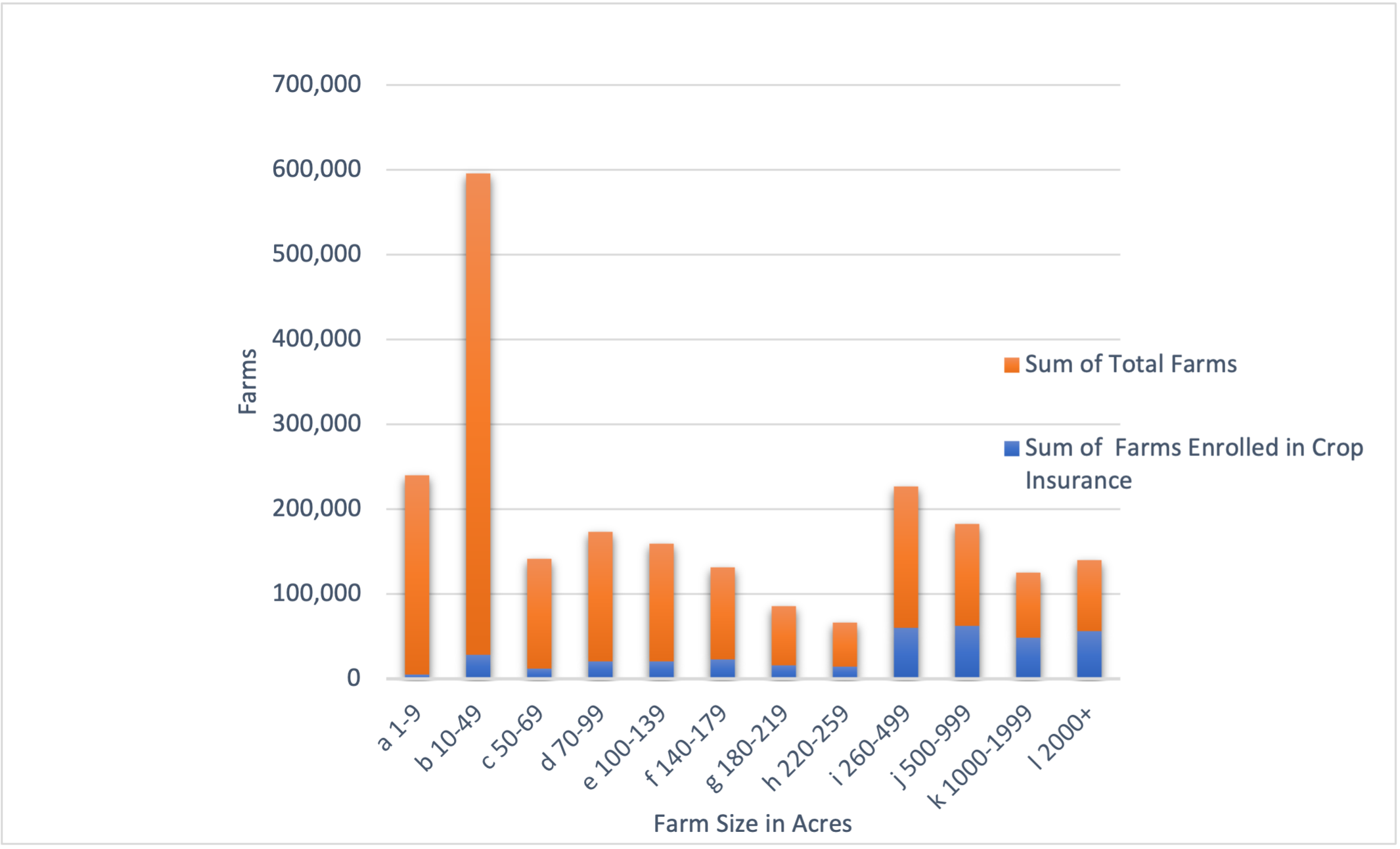

Table 1: Federal Crop Insurance Enrollment[5]

This is because, in the world of crop insurance, particularly row cropping, aggregate benefits are an economy of scale. In the first place, larger farms are more likely than smaller farms to be enrolled in federal crop insurance.[6] But also baked into the system, the statute authorizes the federal government to pay a portion of producers’ premiums and sets subsidy percentages based on coverage level, not farm size.[7] While not inherently unfair because of its uniformity with respect to the level of coverage chosen, total federal support for premium subsidies increases in scale with the number of acres insured.[8] For example, if two farms have the same coverage level, and their premiums are $100/acre of which 50% is subsidized, but one farm is 100 acres, and the other is 1,000 acres, the following would occur:

100 ac. x $100 = $10,000 x 50% = $5,000 aggregate benefit

1,000 ac. x $100 = $100,000 x 50% = $50,000 aggregate benefit.

Thus, the aggregate benefit received by the 1,000-acre farm is substantially larger. In addition, “unlike other farm programs that have income or payment limits, the crop insurance program does not have similar restrictions, so wealthy farmers can get millions in federal subsidies to cover the cost of their insurance, regardless of their income.”[9]

On the whole, the policy design has led to disproportionate consequences. In 2022, “fifty-seven percent of policyholders (263,804 of 460,615) accounted for seven percent of premium subsidy dollars [. . .], with an average premium subsidy of about $3,200 per policyholder.”[10] Inversely, “[a]bout one percent of policyholders (5,537 of 460,615) accounted for twenty-two percent of premium subsidy dollars [. . .], with an average of $464,900 per policyholder.”[11]

Crop insurance also has consequences for land prices and borrowing at a time when most small family farms run on tight margins and are considered high risk by the USDA.[12] First, there is a positive correlation between land prices and federal crop insurance.[13] This is likely from the decreased risk associated with insured crops,[14] not to mention the attractiveness of reduced insurance premiums because of the subsidies. It also undergirds farm credit markets and is often a requirement for farmers to secure favorable loans.[15] Bearing in mind the higher proportion of large farms enrolled in the program, it stands to reason that not only are large farms able to reap the benefits when applying for loans, but large farms are consequently less risk-averse and less at risk of financial ruin than small farms, making them more immune to inflated land prices.

From this, it is easy to deduce potential side effects: land consolidation, risk-taking, and a decrease in accessibility for new farmers to get established. In any case, it is clear that until federal crop insurance behaves more like traditional insurance, acting as a safety net while discouraging risk taking, large farms will continue to disproportionately benefit at the cost of small farms, which the 1933 Farm Bill and 1938 Federal Crop Insurance Act were designed to help. Subsidy caps on high-income and large farms would be a good place to start.

[1] Chad G. Marzen, The 2018 Farm Bill: Legislative Compromise in the Trump Era, 30 Fordham Env’t. Law Rev. 49, 52 (2019).

[2] Id.

[3] Federal Crop Insurance Act, 7 U.S.C. § 1502 (a) (2025).

[4] Andrea Freeman, The 2014 Farm Bill: Farms Subsidies and Food Oppression, 38 Seattle U. L. Rev. 1271, 1272 (2012) (citing 7 U.S.C. §§ 9016 – 9017).

[5] See infra note 6.

[6] U.S. Dep’t of Agriculture, 2022 Census of Agriculture (2022), https://www.nass.usda.gov/Publications/AgCensus/2022/Full_Report/Volume_1,_Chapter_1_US/usv1.pdf [https://perma.cc/X8AL-M7GT].

[7] 7 U.S.C. § 1508 (e) (2025).

[8] Id.

[9] Madeleine Ngo, Large Farmers Received Millions in Insurance Subsidies, Report Says, The New York Times (Dec. 4, 2023), https://www.nytimes.com/2023/12/04/us/politics/crop-insurance-report.html [https://perma.cc/Q47T-69WA].

[10] U.S. Gov’t Accountability Office, Crop Insurance Update on Opportunities to Reduce Program Costs, (2023) https://www.gao.gov/assets/d24106086.pdf [https://perma.cc/4EG3-WYW3].

[11] Id.

[12] Katherine Lacy, et. al., Most Small Family Farms are at High Financial Risk Based on Operating Profit Margin, U.S.D.A. (2024), https://www.ers.usda.gov/data-products/charts-of-note/chart-detail?chartId=108317#:~:text=Home-,Most%20small%20family%20farms%20are%20at%20high,based%20on%20operating%20profit%20margin&text=Small%20family%20farms%20were%20more,Resource%20Management%20Survey%20(ARMS) [https://perma.cc/PNP3-7URH].

[13] Michael Duffy, Impact of Crop Insurance on Land Value, Center for Rural Affairs (2016) https://www.cfra.org/sites/default/files/publications/impact-of-crop-insurance-on-land-values.pdf [https://perma.cc/9CYN-RFUT].

[14] Id.

[15] Stephanie Rosch, Federal Crop Insurance: A Primer, Congressional Research Service (2021) https://www.congress.gov/crs_external_products/R/PDF/R46686/R46686.1.pdf [https://perma.cc/5S5R-457B].